[Case 01]

Targeting 40% of UK that is Financially Vulnerable

FinTech & InsurTech

Driving Inclusion Through AI Driven Future Protection

Faced with growing demand to address the needs of underserved populations, I designed and developed ethical AI for insurance to build trust and mitigate bias amongst the vulnerable who distrust financial institutions.

[Project Overview]

Faced with growing demand to address the needs of underserved populations, I designed and developed ethical AI for insurance to build trust and mitigate bias amongst the vulnerable who distrust financial institutions.

[Problem Statement]

Traditional insurance models fail to address the needs of underserved populations and younger generations who prioritise mental health and intangible assets.

There is an opportunity to develop ethical AI and audit algorithmic data input, so that insurers can build trust by mitigating bias, enhancing transparency, and expanding coverage to include intangible assets.

[Industry]

FinTech / InsurTech

[My Role]

Lead Designer

[Platforms]

Desktop

[Timeline]

January 2025- May 2025

[The Barriers]

Young Parents feel punished by Insurance Algorithms

Traditional insurance treats parenting as “lifestyle choice” vs. essential labor

Community Trust > Corporate Policies

Members of various communities mentioned that "our food bank knows my name. My insurer knows my credit score.”

[Identifying The Underserved]

[Understanding Actuarial Science]

[1] Demographic Data

Used to predict life expectancy and health risks.

Minorities historically underrepresented or misrepresented in datasets.

Led to biased outcomes.

[2] Health & Medical History

Often excluded or face prohibitively high premiums.

Emerging use of genetic data.

Raises ethical concerns

[3] Socio-economic Factors

Stable income earners are prioritised.

Geographic data influences risk assessments.

Disproportionately affect low-income communities.

[4] Behavioural Data

Wearable devices and apps provide real-time data on physical activity, sleep patterns, and stress levels..

Telematics devices track driving behaviour.

Does this determine auto insurance premiums?

Potential for algorithmic bias? Data fails to account for non-traditional family structures, gig workers, or individuals without assets.

Concerns about data misuse and lack of consent. Consumers often lack clarity on how their data is used to calculate premiums.

Focus on Tangible Assets. Short-term focus fails to account for long-term societal shifts.

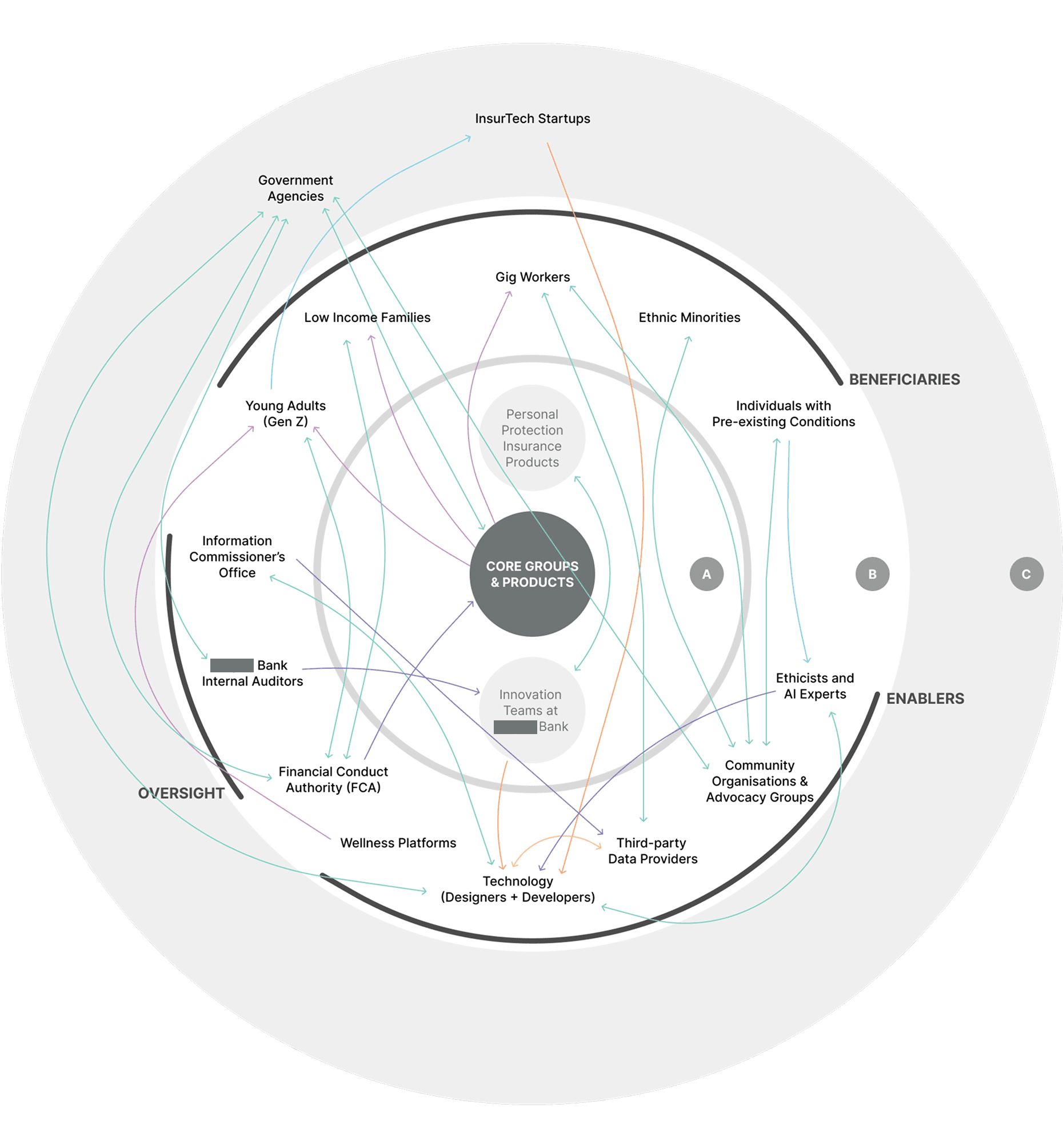

[Stakeholder Map]

[So What?]

Algorithmic Bias

Trust Gap

Algorithmic Biases

AI Bias in Insurance

Distrust

Mental Health Centric

Cultural Trust Gap:

Ethnic minorities and underserved populations lack trust in financial institutions due to cultural barriers, systemic biases, and historical exclusion.

Information Transparency:

Ensuring transparent practices in data usage, mitigating algorithmic bias in claims processing and customer interactions.

Insuring the Intangible:

Expanding insurance coverage to include intangible assets like mental health, sentimental relationships, or skills that hold personal value but are traditionally excluded from conventional policies.

Addressing the Cultural Trust Gap requires inclusive practices.

Information Transparency ensures equitable treatment through unbiased algorithms and transparent processes.

Insuring the Intangible promotes inclusivity by recognising diverse forms of value beyond traditional assets.

Synthesised Opportunity:

Traditional insurance models fail to address the needs of underserved populations and younger generations who prioritise mental health and intangible assets.

There is an opportunity to develop ethical AI and audit algorithmic data input, so that insurers can build trust by mitigating bias, enhancing transparency, and expanding coverage to include intangible assets.

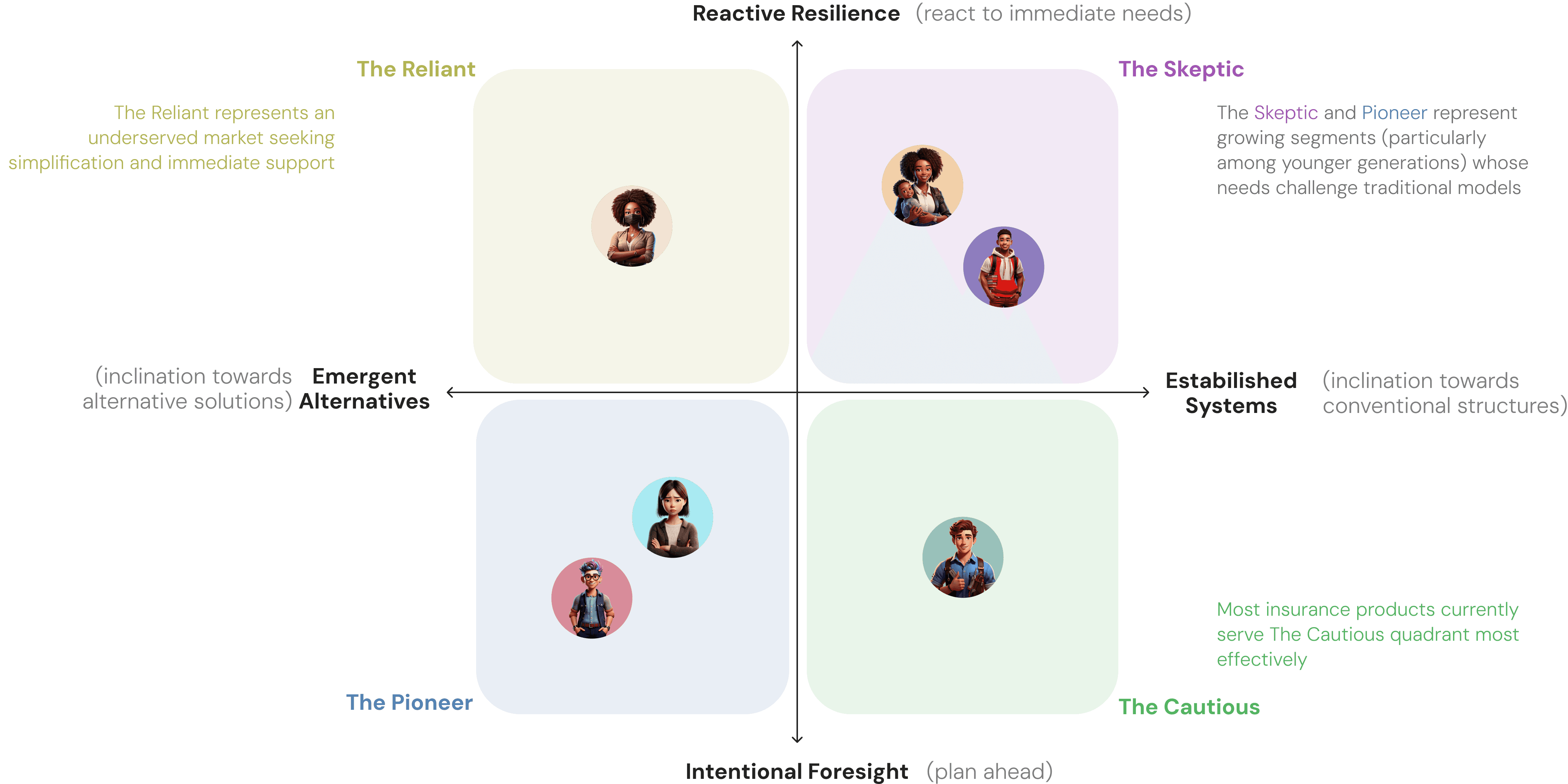

[Archetype]

The Overlooked Caregiver

“A young parent balancing childcare, work, and debt.”

Tech Proficiency: Moderate

The Skeptic

[Attitudes & Needs]

I see insurance as a necessity but view it as unaffordable or inaccessible due to my immediate financial pressures.

I need affordable, flexible coverage that considers caregiving, with clear, non-condescending education on insurance benefits.

[Financial Behaviour]

I rely on immediate income sources like gig/contract work; budgets tightly and may prioritise family needs over personal insurance.

The Precarious Hustler

“Urban worker with volatile income.”

Tech Proficiency: Moderate

The Cautious

[Attitudes & Needs]

I recognise need for protection but am sceptical of traditional insurance due to its lack of flexibility and perceived biases.

I seek on-demand, transparent, and ethical insurance for financial stability amid income volatility.

[Financial Behaviour]

I manage my income through digital platforms and might be open to insurance models in gig apps.

The Unbanked Student

“First-gen university student from minority backgrounds.”

Tech Proficiency: High

The Skeptic

[Attitudes & Needs]

I value security but lack trust in insurance due to family experiences; curious about future financial planning.

I prioritise mental health, affordable insurance, and transparent, ethical education.

[Financial Behaviour]

I manage my finances frugally, combining part-time income with family support; seeking guidance from peers or mentors.

The Data-Skeptical Creative

“Young artist/creative worker concerned about data handling and privacy.”

Tech Proficiency: High

The Pioneer

[Attitudes & Needs]

I see privacy as paramount and question the trustworthiness of a data-driven risk assessment.

I look for transparent and user-controlled insurance solutions that protect my personal and creative assets.

[Financial Behaviour]

I may experiment with AI or community-based financial tools; but not at the expense of my data security and privacy.

The Algorithmic Outsider

“Chronic illness patient flagged as "high-risk" by AI underwriting.”

Tech Proficiency: Moderate

The Reliant

[Attitudes & Needs]

I feel unfairly targeted and discriminated against by algorithm-based systems.

I demand transparency in the way my insurance data is handled and want fair access to coverage.

[Financial Behaviour]

I diligently track my expenses and advocate for consumer rights and data privacy.

The Trust-Deficient Strategist

“Ethnic minority parent.”

Tech Proficiency: High

The Pioneer

[Attitudes & Needs]

I prefer community-based, reciprocal financial arrangements because I lack trust in mainstream institutions.

I requires insurance models that align with my cultural values, offer immediate financial relief, and foster collective resilience.

[Financial Behaviour]

I participate in rotating savings groups or micro-lending initiatives; value community support.

[Engaging With The Vulnerable]

I conducted an engagement with over 20 young parents from minority backgrounds who balance childcare, work and debt.

I used the metaphor of a kitchen and recipe making to take away the stress of being in a situation where they are being vulnerable, and turn it into a game instead. This was key to ensure that I was able to get genuine responses/reactions from them and understand their concerns at a deeper level than simply conducting user interviews.

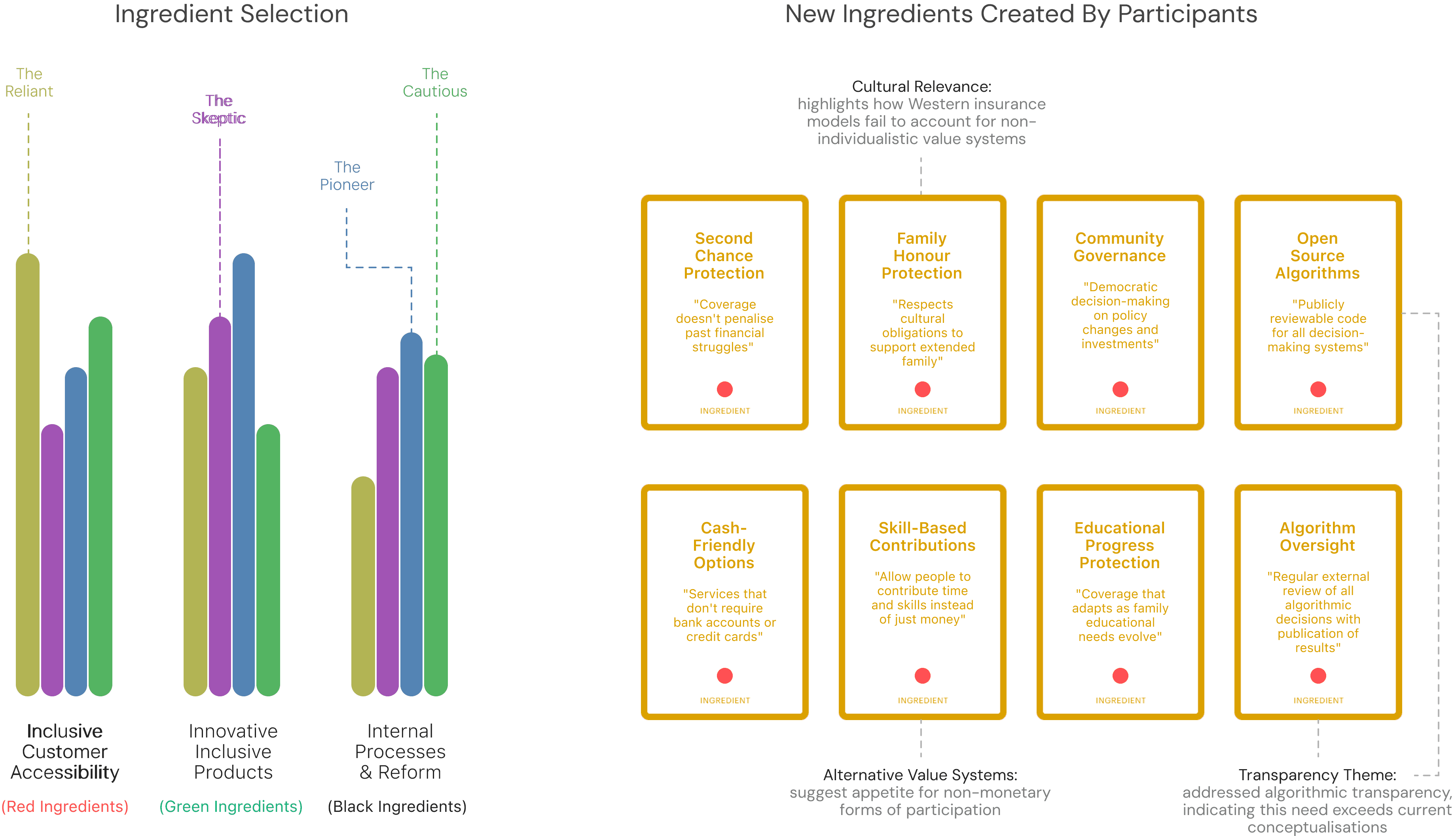

[Engaging With [Name Redacted] Bank]

In this engagement, I shared my findings from the archetypes, distributed the 6 critical internal processes at [Name Redacted] Bank that they (the archetypes) most resonated with, co-created an impact-transparency matrix and identified high-priority processes. This led to further discussions about identifying the biggest barriers to implementing these processes and reform ideas.

[Service Blueprint]

This is how the current service blueprint (a zoomed-in section of the complete blueprint) looks in the initial stages, where a person sees a need for insurance and proceeds to go through the application process. The research so far highlights that there are 2 key points of clarity that need to be tackled.

[Breaking the Chains of Corporate Inertia]

Community trust requires structural separation from legacy systems

[Insight 1]

If we embed our initiatives in large banks, it often becomes diluted by profit priorities.

Marginalised groups tend to distrust corporate-led "social impact" initiatives

[Insight 2]

Banks move slowly on algorithmic and community centred reforms due to legacy compliance frameworks.

[Insight 3]

Experimental initiatives risk reputational damage to parent organisations.

[Insight 4]

Hierarchical banks struggle with radical inclusion.

[Outcome]

Unicorn gives voice and agency to those left out of insurance, building trust through community-driven standards and transparent, people-first innovation.

Unicorns symbolise something exceptional and transformative, perfectly capturing our organisation's unique position at the intersection of ethics and community-led insurance. The unicorn transcends cultural boundaries, appearing in mythologies across diverse cultures, aligning with our goal to serve underrepresented communities.

At Unicorn, we know real change starts with the people who live it every day. That’s why we onboard communities as official Unicorn Communities - giving them a seat at the table, not just a voice on the sidelines. We listen, understand, and co-create protection solutions side by side with those we serve. We believe in rewarding those who lift up their neighbourhoods - so when you give back, you earn more than gratitude; you earn Unicorn Credits that make your protection more affordable.

[Demographic Blind Quotation System]

Unicorn gives voice and agency to those left out of insurance, building trust through community-driven standards and transparent, people-first innovation.

Unicorns symbolise something exceptional and transformative, perfectly capturing our organisation's unique position at the intersection of ethics and community-led insurance. The unicorn transcends cultural boundaries, appearing in mythologies across diverse cultures, aligning with our goal to serve underrepresented communities.

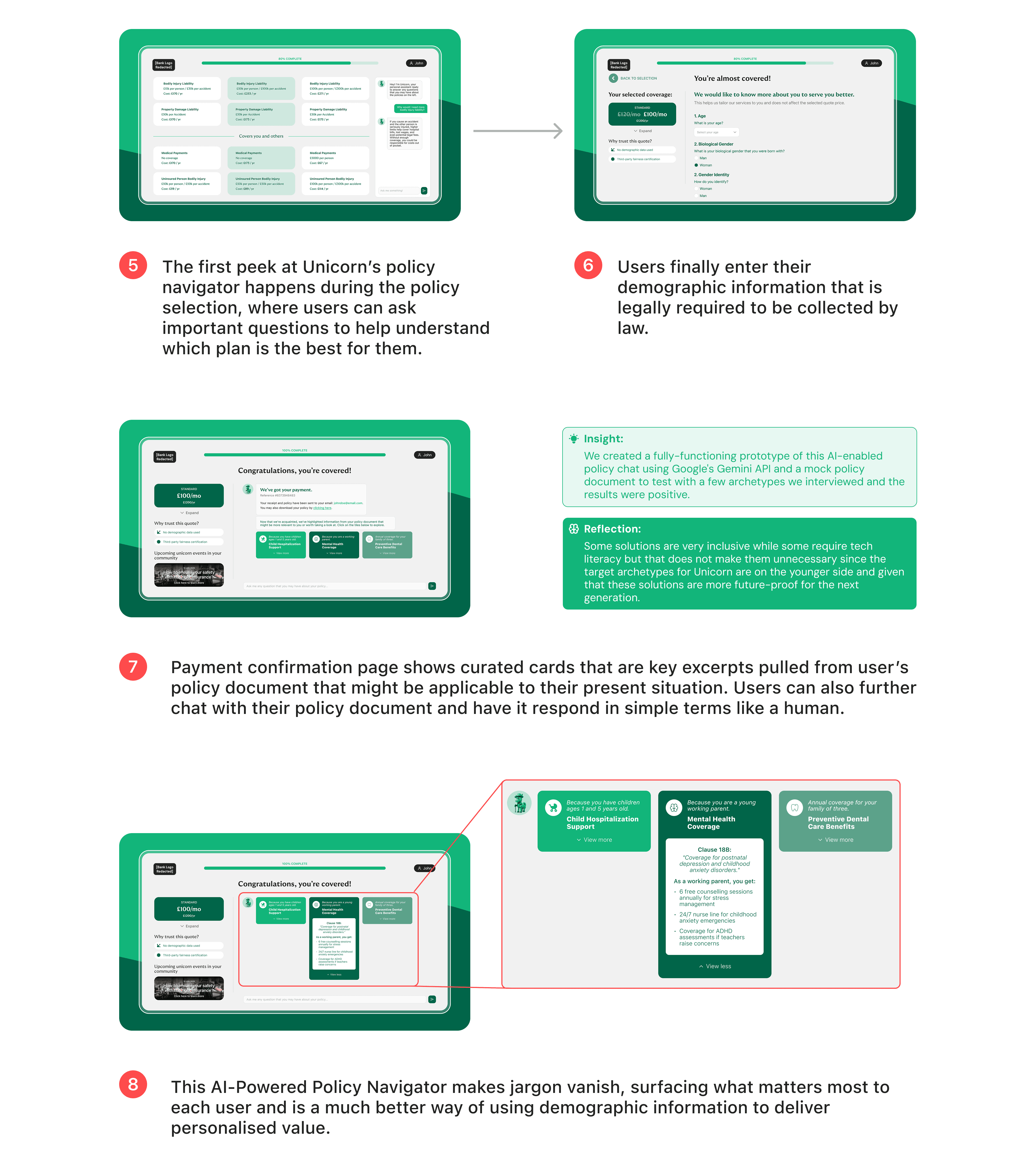

[AI Powered Policy Navigator]

Unicorn gives voice and agency to those left out of insurance, building trust through community-driven standards and transparent, people-first innovation.

Unicorns symbolise something exceptional and transformative, perfectly capturing our organisation's unique position at the intersection of ethics and community-led insurance. The unicorn transcends cultural boundaries, appearing in mythologies across diverse cultures, aligning with our goal to serve underrepresented communities.

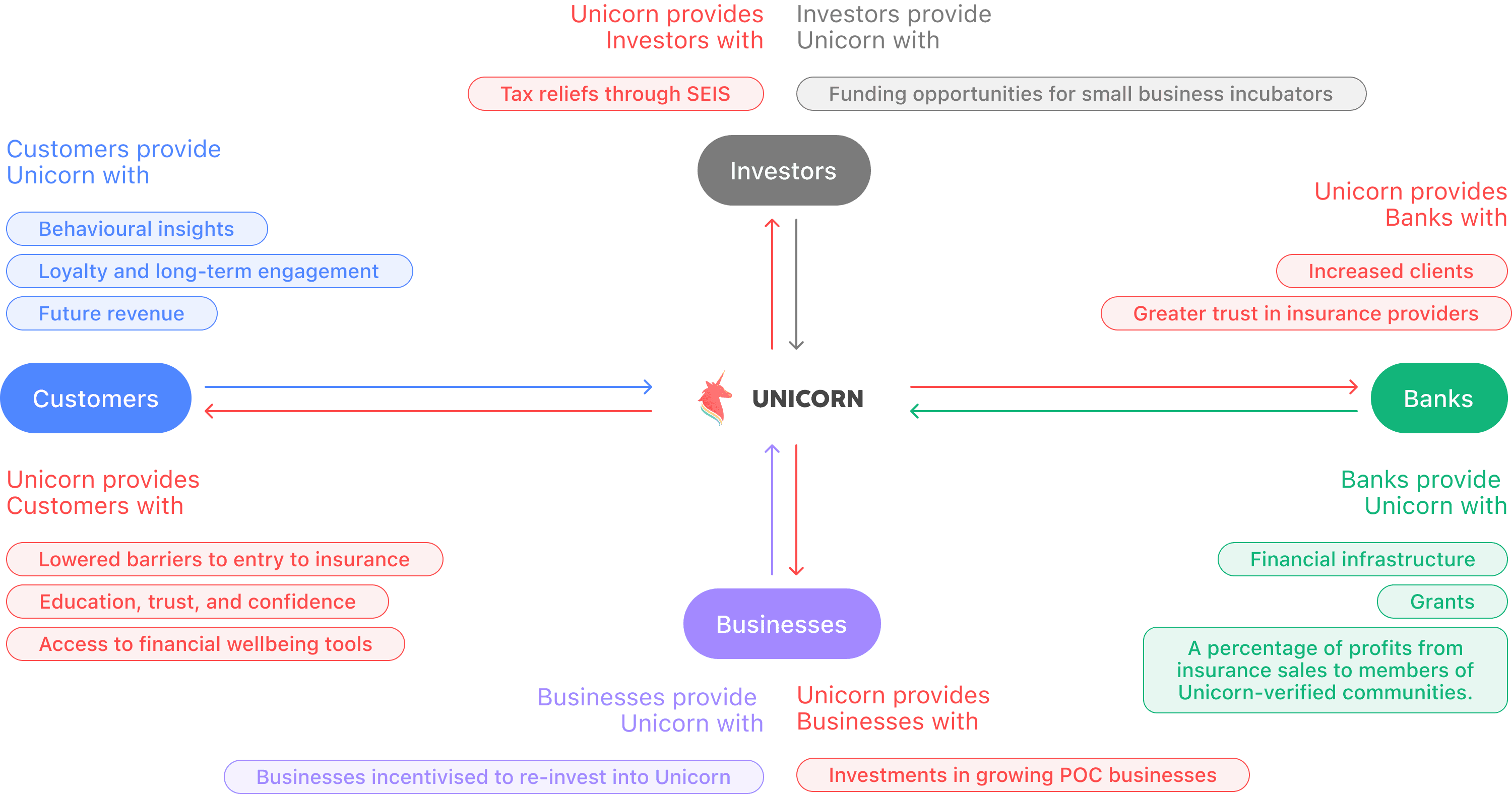

[Value Exchange Ecosystem]

I'm not building a product. I'm building a system of trust. One where every participant is better off because they’re part of it. This is not a zero-sum game, it’s a compounding loop of value. And Unicorn is the conductor.

[Key Learnings]

Power Dynamics

While we created community partnerships, we must acknowledge that true power redistribution requires continuous vigilance-how might Unicorn avoid reproducing existing hierarchies over time?

Personal Design Growth

I learned to design within, rather than simplifying away from, the complex realities of marginalisation and financial exclusion.

Pluriversal Possibility

Could truly radical approaches have emerged by starting not with "how to fix insurance" but with "how communities already protect each other"? The project begins from institutional rather than communal frameworks. However, this is not easy to do as well due to the project stakeholder bring [Name Redacted] bank which naturally reinforces a different approach to the problem.